E Kpss Test Kitaplarý

2020 Ekpss Zihinsel Engelli Tum Adaylar Icin Genel Tarama Soru Bankasi Paragon Yayincilik 9786056960475

2020 E Kpss Genel Yetenek Ve Kultur Tum Dersler Soru Bankasi Uzman Kariyer Yayinlari 9786053298946

Yargi Yayinlari 2020 Ekpss Tum Adaylar Konu Kitabi Soru Bankasi Seti Uygunkitapal

Ekpss Yaprak Test Sahide Korkmaz Nbsp Kpss Oabt Ales Dgs Yks Lgs Yds Gys Aof Kitaplari

Ekpss Cikmis Sorular Kaynak Kitaplari Palme Kitabevi

Ekpss Kitap Fiyatlari Ve Modelleri Hepsiburada

1 level 0 216000 5 level 0 146000 10 level 0 119000 please answer.

E kpss test kitaplarý. The p value is less than 0 05. Is it stationary or not also when take differences of series first and second still not under the critical value of 5. Kwiatkowski phillips schmidt shin test statistic value is less than any of the below than we would accept the null i e the variable is stationary. Computes the kwiatkowski phillips schmidt shin kpss test for the null hypothesis that x is level or trend stationary.

A function is created to carry out the kpss test on a time series. By testing both the unit root hypothesis and the stationarity hypothesis one can distinguish series that appear to be stationary series that appear to have a unit root and series for which the data or the tests are not sufficiently informative to be sure whether they are stationary or integrated. This is white noise around a trend so it is definitely a stationary process but has a trend. Test the hypothesis that the log wages series is a unit root process with a trend i e difference stationary against the alternative that there is no unit root i e trend stationary.

I m using r to calculate the kpss to check the stationarity. Wnt kpss level 2 1029 truncation lag parameter 4 p value 0 01. Time series econometrics eviews kpss test. Kpss test kpss is another test for checking the stationarity of a time series.

The series has a unit root series is not stationary. Conduct the test by setting a range of lags around t as suggested in kwiatkowski et al 1992. The process is trend stationary. The library that i m using is tseries and the function is kpss test.

The null hypothesis of stationarity around a level is rejected. I have done a simple test using cars a default matrix on r. Kpss test for level stationarity data. In kpss test critical value is passing from 1 but not from 5 so.

Kpss type tests are intended to complement unit root tests such as the dickey fuller tests. Türkiye nin hocaları sizin yanınızda kitap satışımız için.

E Kpss

Yargi Yayinlari 2020 E Kpss Tum Adaylar Icin Konu Kitabi

Yargi Yayinlari 2020 E Kpss Tum Adaylar Icin 10 Deneme Sinavi

E Kpss

Yediiklim Yayinlari 2020 Kpss Lise Onlisans Tum Dersler Cek Kitabi

Ekpss Soru Bankasi Deneme Konu Anlatimi Kitap Secenekleri

Benzer Mi Ne Tyt Yks Kpss Dgs Facebook

Adana Icinde Ikinci El Satilik Kpss Test Kitaplari Letgo

2020 Kpss Tarih Kupa Konu Konu Test Bankasi Uzman Kariyer Yayinlari 9786053298663

Kitappaketi Kitap Mi Paketiniz Hazir

100 Yil Icindeki Ucretsiz Kpss Test Kitaplari Ihtiyaci Olan

Ekpss Kitap Fiyatlari Ve Modelleri Hepsiburada

2020 Kpss Lise On Lisans Gy Gk Soru Denizi Cek Kopartli Yaprak Test Komisyon Nbsp Kpss Oabt Ales Dgs Yks Lgs Yds Gys Kitaplari Pegem Net Internetteki Kitapciniz

Kpss Kpss Hazirlik Kaynak Kitaplari Kidega Kitap Kategorisinde

Isem Kitap Isem 2021 Evveliyat Kpss Genel Kultur Tarih Cek Kopar Yaprak Test Trendyol

Kpss Ortaogretim Genel Kultur Genel Yetenek Data Yay Test Kitaplari Sahibinden Com Da 871348828

Ekpss Kitaplari Bkmkitap Com

2020 Ekpss Tum Adaylar Icin 10 Deneme Sinavi Yargi Yayinlari 9786052842546

Yargi Yayinlari 2020 Kpss Genel Yetenek Matematik Cek Kopartli Yaprak Test

Metin Sar Kpss Egitim Facebook

Lise Onlisans Kitaplari 30 Indirim

Sayi Problemleri Test 31 Matematigin Kara Kutusu Yks Tyt Ayt Kpss Dgs Youtube

Avrupa Kitap Dagitim

Pegem 2020 Kpss Full Set At Sahibinden Com 880277520

Ekpss Kitaplari Bkmkitap Com

Destek Kitap

2016 Ekpss Icin Calisma Kitaplari Listesi Is Dunyasinda Ben De Varim Com

Hedef 2020 Kpss Genel Yetenek Genel Kultur Cek Kopar Yaprak Test K

Avrupa Kitap Dagitim

Tum Ekpss Engelli Sinavi Kitaplari Konu Anlatimlar Denemeler Yaprak Testleri Ve Setler

Kitappaketi Kitap Mi Paketiniz Hazir

2020 Kpss Genel Kultur Cek Kopart Yaprak Test Kollektif Kitapyurdu Com

Destek Kitap

Kpss 2020 Kitap Onerileri

Mev Ken Kirtasiye Home Facebook

Hudavendigar Icinde Ikinci El Satilik Yargi Kpss Lisans Tes

Yeni Trend Yayinlari 2020 Kpss Lise On Lisans Tarih Yaprak Test Komis

Kpss Matematik Soru Kitabi Uzman Kariyer Test Kitaplari Sahibinden Com Da 889963564

Yediiklim 2021 Kpss Egitim Bilimleri Pratik Serisi Soru Bankasi Tek Kitap Yediiklim Yayinlari Indekskitap Com

Tum Ekpss Engelli Sinavi Kitaplari Konu Anlatimlar Denemeler Yaprak Testleri Ve Setler

Avrupa Kitap Dagitim

2021 Kpss Egitim Bilimleri Gelisim Psikolojisi Cek Kopart Yaprak Test Komisyon Kitapyurdu Com

Destek Kitap

Kpss Kaynak Tavsiyeleri 2020 Kpss Kitap Tavsiyesi Kpss Lisans Kullandigim Kaynaklar Youtube

Kpss Sinava Hazirlik Test Ve Konu Anlatim Kitaplari Indirimli 34 Sayfa

0 Dan 8 E Sayisal Konu Anlatimli Soru Bankasi Komisyon Nbsp Kpss Oabt Ales Dgs Yks Lgs Yds Gys Kitaplari Pegem Net Internetteki Kitapciniz

Evrensel Iletisim 8 Sinif Lgs Ye Hazirlik Telafi Test Kitabi Video Co

8 Sinif Lgs Cep Test Seti 7 Kitap Karekok Yayinlari

Dhbt 2020 Tafsilat 10 Cozumlu Deneme Tum Adaylar Icin Test Kitabi Orta Ogretim Onlisans Lisans Mehmet Umutli Yedi Beyza Yayinlari Hazirlik Diyanet Isleri Baskanligi Osym Imam Hatip Kpss Sinav Kitabi Satis Siparis

Pdf The Effect Of Solution Focused Brief Counseling On Reducing Test Anxiety

Uzman Kariyer 2020 Kpss Genel Yetenek Genel Kultur Kupa Test Bankasi Yaprak Test 5 Li Set Uzman Kariyer Yayinlari Indekskitap Com

Tonguc Akademi 3 Sinif 0 Dan 3 E Tum Dersler Konu Anlatimli Soru Bankasi Kitapisler Isler Kitabevleri

Yargi Yayinlari 2020 Kpss Lise On Lisans Gy Gk Konu Soru 10 Deneme Yaprak Test Cikmis Soru Seti Uygunkitapal

Lgs Lise Tyt Ayt Kpss Dgs Ales Yds Toptan Kitap Al

10 Sinif Matematik Fasikul Soru Kitabi

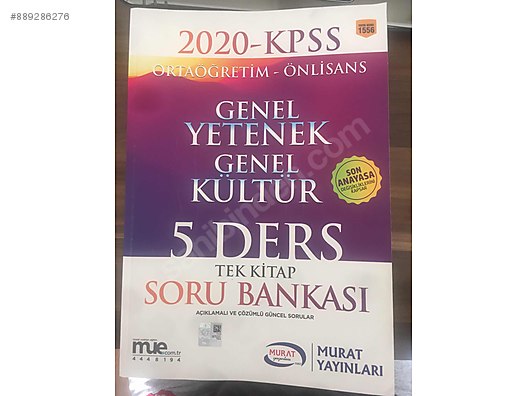

2020 Kpss Soru Bankasi Test Kitaplari Sahibinden Com Da 889286276

Ekpss 54 Soru Deneme Sinavi 2021 Kpss Guncel Bilgiler

Armoni Kitabevleri Home Facebook

6 Sinif Vip Soru Bankasi Seti 5 Kitap Editor Yayinevi Tum Dersler

Gale Academic Onefile Document Dynamics Of Suicide In Turkey An Empirical Analysis Dynamique Du Suicide En Turquie Analyse Empirique

Pratik Hocam Yayinlari Kpss Tarih Kirmizi Kitap Soru Bankasi

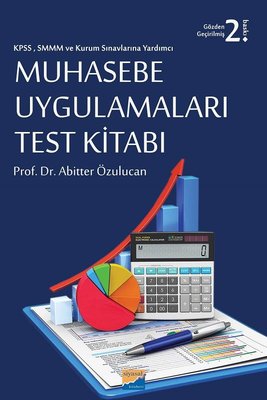

Muhasebe Uygulamalari Test Kitabi D R Kultur Sanat Ve Eglence Dunyasi

Kpss Egitim Bilimleri Gelisim Psikolojisi Yaprak Test Yeni Trend Yayinlari 2020 Savas Kitap Ve Yayinevi

Data Yayinlari

Ekpss Kitaplari Kidega

2020 Kpss Egitim Bilimleri Program Gelistirme Yaprak Test

Turkiye Nin Online Kitap Ve Kirtasiye Magazasi Ucretsiz Kargo Imkani Kapida Odeme

Ingilizce Test Teknikleri Kpds Uds Kpss Toefl Pelikan Tip Teknik Yayincilik E Kitap E Kitap Dunyasi

E Sahaf Ikinci El Kitap Ders Notlari

Test 56 Soru 8 Tamlamalar Soru Cozumu Tyt Yks Kpss Ad Tamlamasi Test Coz Youtube

Ornek Akademi 10 Sinif Tek Kitap Konu Anlatimli Tarama Test Kitabi I Kpssstore Com Kpss Nin Tek Adresi

Yargi Yayinevi 2020 Kpss Genel Kultur Cografya Cek Kopartli Yaprak Test Trendyol

Destek Kitap

2020 Kpss Ortaogretim Soru Ve Cevaplari Aciklandi Osym Ortaogretim Lise Kpss Cevap Kitapcigi Egitim Haberleri

Kpss Matematik Kupa Konu Konu Test 2020

Kpss Kitaplari 2020 2021 Yds Dgs Oabt Ygs Yks Lgs Tyt

Cefr Based Language Testing E Kitap Ozcan Demirel Nbsp Kpss Oabt Ales Dgs Yks Lgs Yds Gys Kitaplari Pegem Net Internetteki Kitapciniz

Hudavendigar Icinde Ikinci El Satilik Yargi Kpss Lisans Tes

Yediiklim Yayinlari Tyt Ayt Kpss Paragraf Cek Kopart Yaprak Test

Baskent Yayin Dagitim

Avrupa Kitap Dagitim

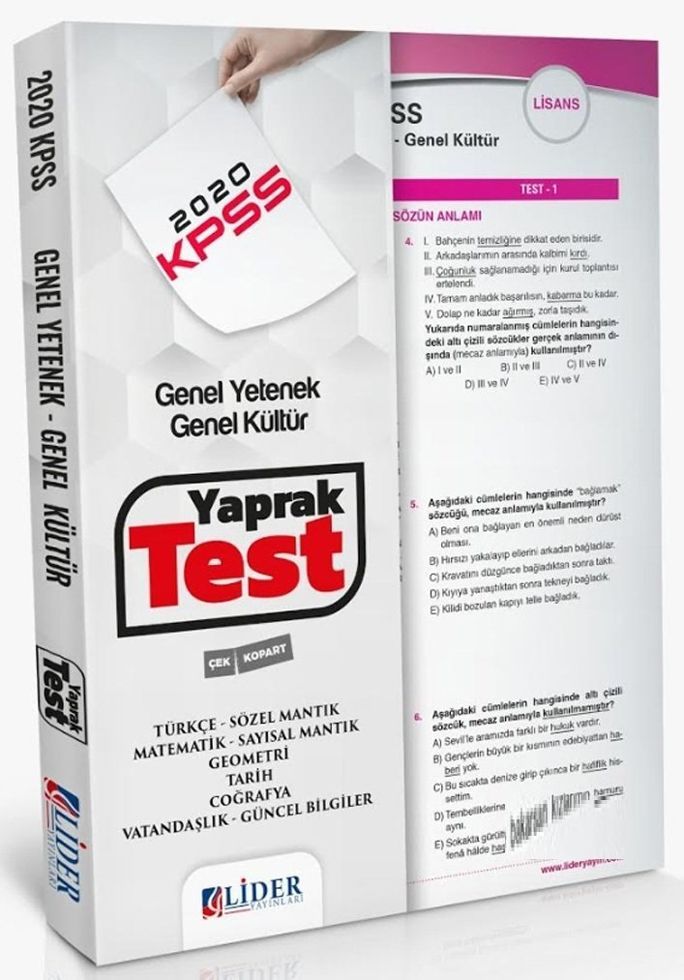

Lider Yayinlari 2020 Kpss Genel Yetenek Genel Kultur Yaprak Test Kpss Yaprak Testler Kitapiste Com Isimiz Gucumuz Kitap

Ekpss Kitaplari Bkmkitap Com

Yediiklim 2021 Kpss Egitim Bilimleri Gelisim Psikolojisi Yaprak Test Cek Kopart Yediiklim Yayinlari Kitappatik Com

Beyaz Kalem Kpss Cografya Yaprak Test Fiyatlari Ve Ozellikleri

Kpss 2020 Soru Bankasi Test Kitaplari Sahibinden Com Da 877993674

Uzman Kariyer 2020 Kpss Genel Yetenek Genel Kultur Tek Kitap Konu Anlatimli Uzman Kariyer

Kitapci Kaliteli Kitap Uygun Fiyat

Yediiklim 2018 Kpss Genel Yetenek Genel Kultur Cek Kopart Yaprak Test Tarafindan Yediiklim Yayinlari Cevrimici Kitaplar

Tum Ekpss Engelli Sinavi Kitaplari Konu Anlatimlar Denemeler Yaprak Testleri Ve Setler

Yargi Yayinlari 2020 Kpss Genel Yetenek Genel Kultur Cek Kopartli Yaprak Test Seti

Apotemi Problemler Test Kitabi Tyt Yks Kpss Ales Dgs Msu Icin Konu Anlatimli Soru Bankasi 9786058152885

1 Sinif Matematik 1 Sinif Matematik Matematik Dergileri Matematik