Kpss Ortaöðretim Test Pdf

Top Pdf Kpss Test 1library

Top Pdf Kpss Test 1library

Pdf A Bootstrap Based Kpss Test For Functional Time Series

Pdf The Kpss Test With Outliers

Top Pdf Kpss Test 1library

Pdf A Bootstrap Based Kpss Test For Functional Time Series

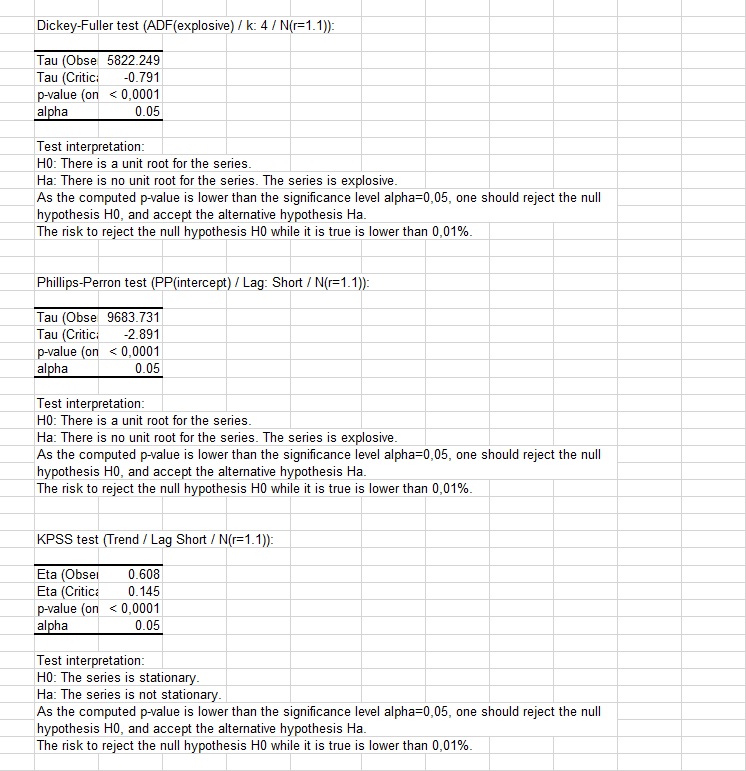

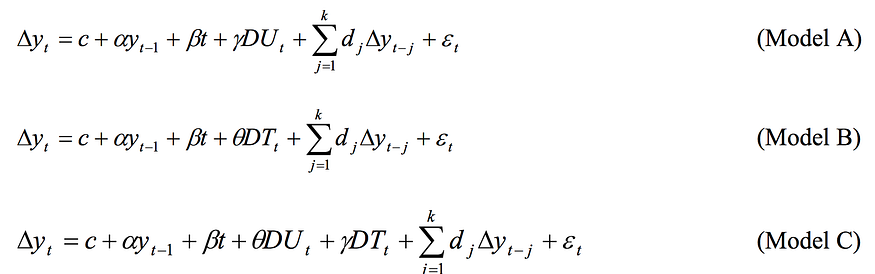

Case 4 reject unit root reject stationarity.

Kpss ortaöðretim test pdf. Both imply that series is stationary. Seasonal kpss test to be extended to include deterministic seasonality. The alternative is the model that. First test for the existence of unit root 1 and second test for the complex roots where the null hypothesis will be specified thereafter.

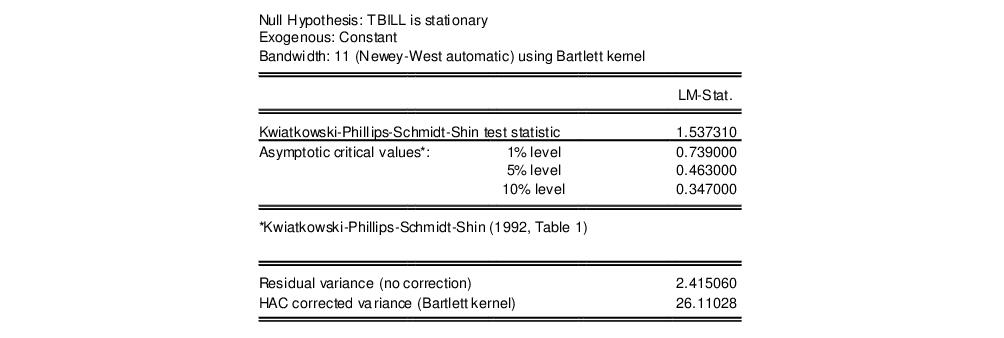

The kpss test of kwiatkowski et al. Adf test is very powerful in time series with outliers but kpss test should use with second thoughts in presence of outliers. A complementary test for the kpss test with an application to the us dollar euro exchange rate ibrahim ahamada greqam université de la méditerranée. Its null hypothesis is that the series follows the model x t t t where f tgis a stationary time series.

Both hypothesis are component hypothesis heteroskedasticity in series may make a big difference. The kpss test has been widely used in macroeconomics and international finance for instance by kuo and mikkola 84 gunduz 85 and tsen 86 to check long run and functional time series for. Our test statistic is a generalization of the kpss test in the sense that it also con siders the partial sum process of the residuals et of each of the following regressions depending on the null hypothesis i e h. We are interested in a one sided lm test rather than a two sided test.

The testing procedure follows in two steps. See e g rogers 19861 1 nyblom and makelainen 1983 give the lb1 statistic for the level stationary case 5 0 of our model. The kpss test with two structural breaks josep lluís carrion i silvestre grup de recerca aqr departament d econometria estadística i economia espanyola universitat de barcelona andreu sansó departament d economia aplicada universitat de les illes balears july 22 2005 abstract in this paper we generalize the kpss type test to allow for two struc tural breaks. Nyblom 1986 considers a model equivalent to our model and gives the lb1 test statistic but a more.

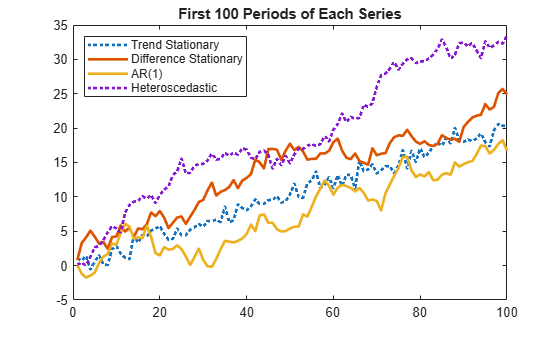

Data give not enough observations. The seasonal kpss test is a lagrange multiplier based test hence the null hypothesis. Kpss test for functional time series piotr kokoszka colorado state university gabriel young colorado state university abstract econometric and nancial data often take the form of a collection of curves ob served consecutively over time. The similar results are also reported by otero and smith 2005.

1992 has become one of the standard tools in the analysis of econometric time series. Examples include intraday price curves term struc ture curves and intraday volatility curves. If there is structural break it will affect inference. Case 3 if we can t reject both test.

Table 1 From The Kpss Test With Outliers Semantic Scholar

Top Pdf Kpss Test 1library

Top Pdf Kpss Test 1library

Table 3 From The Kpss Test With Outliers Semantic Scholar

Pdf The Kpss Test With Two Structural Breaks

Top Pdf Kpss Test 1library

Pdf A Bootstrap Based Kpss Test For Functional Time Series

Top Pdf Kpss Test 1library

Http Www Stat Colostate Edu Piotr Kpssreduced Pdf

Top Pdf Kpss Test 1library

Pdf A Bootstrap Based Kpss Test For Functional Time Series

Eviews Help Unit Root Testing

Doc Kpss Vs Praxis Elif Canan Academia Edu

Top Pdf Kpss Test 1library

Pdf A Bootstrap Based Kpss Test For Functional Time Series

Download All Topik Tests Pdf Answer Audio Update 64th Test Korean Topik Study Korean Online Học Tiếng Han Online

Kpss Test And Model Misspecifications Request Pdf

Top Pdf Kpss Test 1library

Top Pdf Kpss Test 1library

Http Fmwww Bc Edu Ec C S2000 Ec771b Unitroottests Pdf

Top Pdf Kpss Test 1library

Http Leonardo3 Dse Univr It Home Workingpapers Fragility Kpss Pdf

Http Www Mdpi Com 2225 1146 3 2 339 Pdf

Https Www Researchgate Net Profile Christopher Baum2 Publication 24137563 Tests For Stationarity Of A Time Series Update Links 0fcfd50f5ffa1bbbc3000000 Tests For Stationarity Of A Time Series Update Pdf

Top Pdf Kpss Test 1library

Unit Root Dickey Fuller And Stationarity Tests On Time Series Xlstat Support Center

Pdf Application Of Modified Kpss Test With Fourier Analysis In Stationarity Test Of Hydrologic Time Series Case Study Lake Urmia Water Level

Pdf Kpss Stata Module To Compute Kwiatkowski Phillips Schmidt Shin Test For Stationarity

Https Core Ac Uk Download Pdf 143888209 Pdf

Https Zaguan Unizar Es Record 63059 Files Texto Completo Pdf

Http Www Econstor Eu Bitstream 10419 22430 1 Dp 318 Pdf

Https Www Researchgate Net Profile Paul Louangrath Post Is Unit Root Testing Always A Precondition With Time Series Data Attachment 5befeee1cfe4a7645502c5b8 As 3a693903577591808 401542450913181 Download Unit Root 3 Pdf

Https Jennischaefer Com Wp Content Uploads 2013 05 Compulsive Exercise Test Pdf

Https Himayatullah Weebly Com Uploads 5 3 4 0 53400977 Stationarity And Unit Root Testing Qaisar Ayub Attaurrahman Pdf

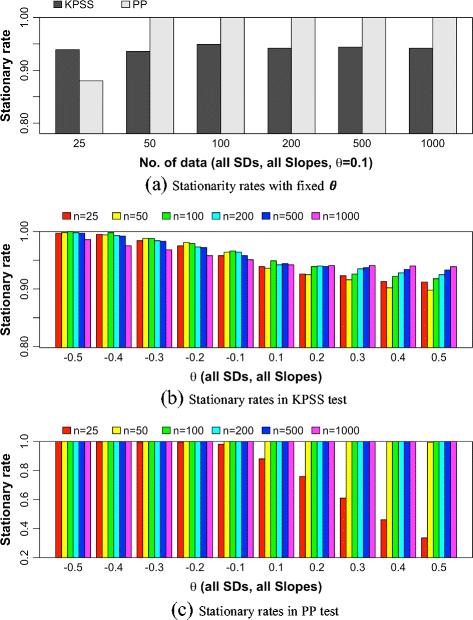

Pdf Empirical Power Of The Kwiatkowski Phillips Schmidt Shin Test Semantic Scholar

Econometrics Beat Dave Giles Blog Unit Root Testing Sample Size Vs Sample Span

Http Coin Wne Uw Edu Pl Lgoczek Pdf Macroeconometrics2 Pdf

Jrfm Free Full Text Expectations For Statistical Arbitrage In Energy Futures Markets Html

Kpss Test Archives Analytics Vidhya

Http Bibliotecadigital Fgv Br Dspace Bitstream 10438 12583 1 1988 Pdf

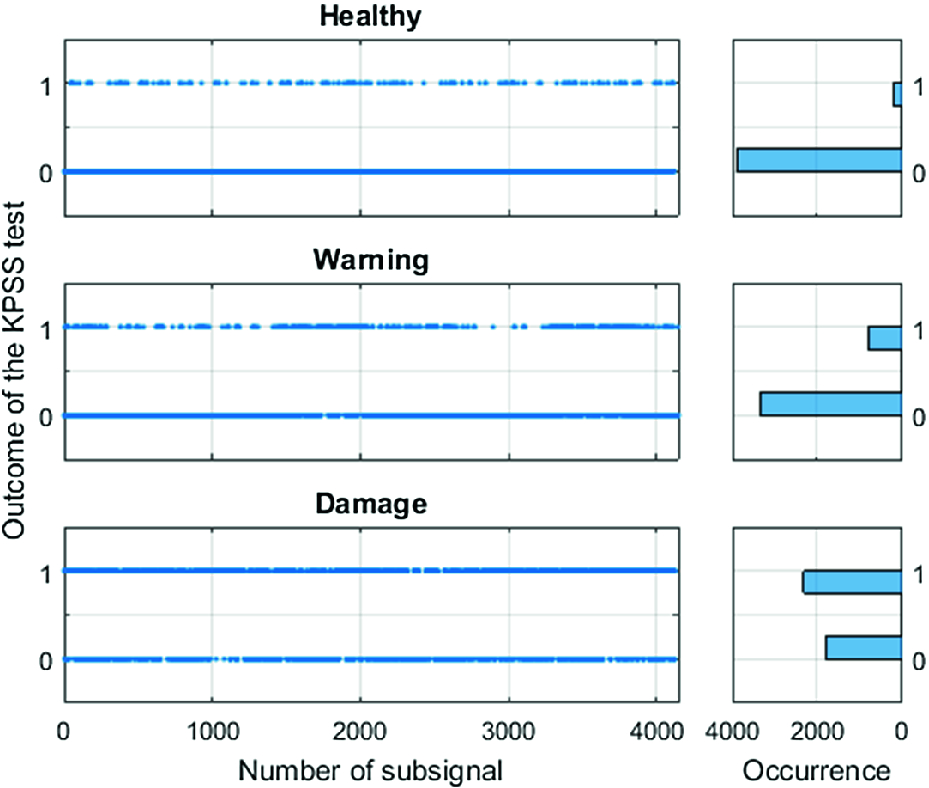

Integration Approach For Local Damage Detection Of Vibration Signal From Gearbox Based On Kpss Test Springerlink

Econometrics Free Full Text The Seasonal Kpss Test Examining Possible Applications With Monthly Data And Additional Deterministic Terms Html

Http Article Sciencepg Net Pdf 10 11648 J Ajtas 20160503 20 Pdf

Https Www Princeton Edu Umueller Stationtestp Pdf

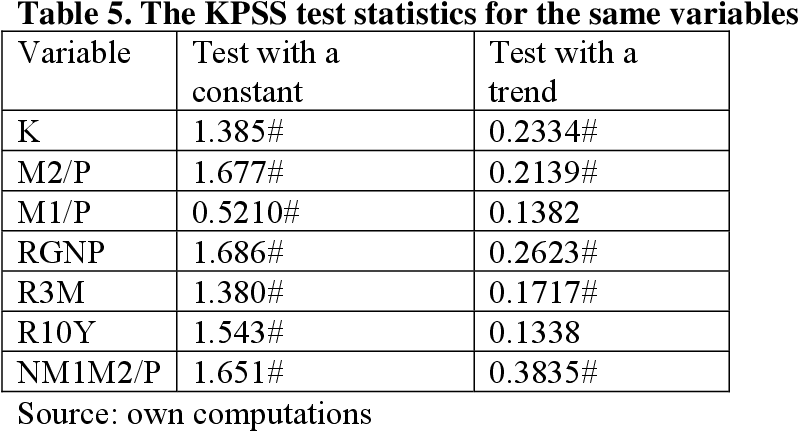

Table 1 Unit Root Tests Kpss Test Augmented Dickey Fuller Test With Time Trend Pdf Free Download

Pdf Using Stationarity Tests In Antitrust Market Definition

On Consistency Of Tests For Stationarity In Autoregressive And Moving Average Models Of Different Orders Science Publishing Group

Journal Of Economics And International Finance The Optimal Forecast Model For Ghana S Inflation A Stochastic Approach

Assess Stationarity Of Time Series Using Econometric Modeler Matlab Simulink

Model Identification Ppt Download

Carbon Price Volatility The Case Of China

Finite Sample Critical Values Of The Generalized Kpss Stationarity Test Springerlink

Https Www Princeton Edu Umueller Lowfreqp Pdf

Https Arxiv Org Pdf 1901 09145

Pdf Testing The Validity Of Purchasing Power Parity For Asian Countries During The Current Float

Http Www Usc Es Economet Reviews Ijaeqs124 Pdf

Pdf Test Retest Reliability Of The Sensory Organization Test In Older Persons With A Transtibial Amputation Prasath Jayakaran Academia Edu

Kpss Test For Stationarity Matlab Kpsstest

Testing The Efficiency Of The Wine Market Using Unit Root Tests With Sharp And Smooth Breaks Sciencedirect

Pdf Selection Of Unit Root Test On The Basis Of Length Of The Time Series And Value Of Ar 1 Parameter

Kpss Test And Model Misspecifications Request Pdf

Http Debis Deu Edu Tr Userweb Onder Hanedar Dosyalar So Pdf

Http Homepage Univie Ac At Robert Kunst Pres Seas12 Zimmermann Pdf

7 Statistical Tests To Validate And Help To Fit Arima Model By Pratik Gandhi Towards Data Science

Pdf Variance Ratio Test And Weak Form Efficiency Of Bahrain Bourse

Download All Topik Tests Pdf Answer Audio Update 64th Test Korean Topik Study Korean Online Học Tiếng Han Online

Http Www Mv Helsinki Fi Home Amoaning Time 20series 20analysis Time 20series 20concept Trendcycle 20decomposition Unit 20root 20test Unitrootlecture2 Pdf

Https Ageconsearch Umn Edu Record 261430 Files Ritter 20m 20yang 20x 20and 20odening 20m 20 2017 20spatial 20integration 20of 20agricultural 20land 20markets Pdf

Pdf The Effect Of The Stock Exchange On Economic Growth A Case Of The Zimbabwe Stock Exchange Semantic Scholar

Unit Root Testing Arch 4 15 2 Gd5f5b5bc Documentation

Https Content Sciendo Com Downloadpdf Journals Jses 8 2 Article P24 Pdf

Https Www Researchgate Net Profile Christopher Baum2 Publication 24096639 Stata The Language Of Choice For Time Series Analysis Links 543d6cfa0cf240f04d10c153 Stata The Language Of Choice For Time Series Analysis Pdf

Http Udsspace Uds Edu Gh Bitstream 123456789 623 1 Effects 20of 20rice 20importation 20on 20the 20pricing 20of 20domestic 20rice 20in 20northern 20region 20of 20ghana Pdf

Https Www Monash Edu Data Assets Pdf File 0003 925680 Unit Root Properties Of Natural Gas Spot And Futures Pricesthe Relevance Of Heteroskedasticity In High Frequency Data Pdf

Https Support Sas Com Resources Papers Proceedings15 3294 2015 Pdf

Determining The Stationarity Distance Via A Reversible Stochastic Process

Pdf Fdi And Economic Growth Relationship An Empirical Study On Malaysia

Detecting Stationarity In Time Series Data

Unit Root Tests Matlab Simulink

Https Www Jstor Org Stable 23243807

Testing For Regional Convergence Of Agricultural Land Prices Sciencedirect

Https Www Jstor Org Stable 40664501

Tutorial Statistical Tests Of Hypothesis Data Science Central

Https Www Jstor Org Stable 2284962

Eviews Seasonal Unit Root Tests

Pdf Is Real Gdp Stationary Evidence From Some Unit Root Tests For The Advanced Economies

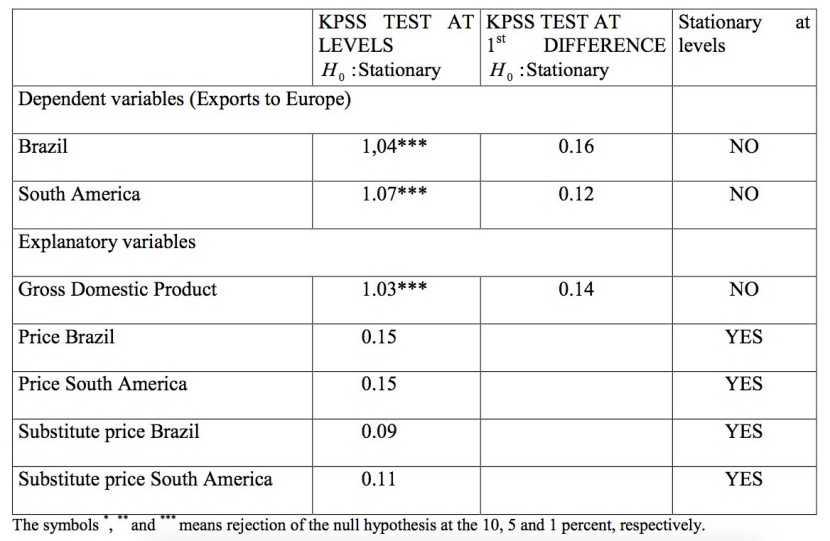

Dynamics Of Pulp Exports From South America To The European Union

Performance Evaluation Of Four Statistical Tests For Trend And Non Stationarity And Assessment Of Observed And Projected Annual Maximum Precipitation Series In Major United States Cities Springerlink

Https Arxiv Org Pdf 1901 02714

Https Cran Microsoft Com Snapshot 2017 09 17 Web Packages Tseries Tseries Pdf

Https Www Econjournals Com Index Php Ijefi Article Download 29 Pdf

Pdf Testing The Weak Form Of Efficiency Of Cryptocurrencies A Case Study Of Bitcoin And Litecoin

The Unit Root Tests Arch 4 15 2 Gd5f5b5bc Documentation